💡 Mastering Your Retirement Corpus: The Definitive Guide to EPFO Schemes and Seamless Fund Withdrawals

A comprehensive guide to understanding EPFO's EPF, EPS, and EDLI schemes, managing your UAN, and navigating the online withdrawal process for a secure retirement.

EPFO is one of the most important savings systems for salaried employees in India. If you are working in a private or government job, a part of your salary automatically goes into EPF every month. Many people see this deduction but don’t fully understand how it actually builds retirement savings over time. At its core, the EPFO manages a mandatory savings system where both you and your employer contribute a portion of your monthly salary to build a substantial retirement fund. This system is not just a single savings account; it is a tripartite framework consisting of the Employees' Provident Fund (EPF) for wealth accumulation, the Employees' Pension Scheme (EPS) for post-retirement income, and the Employees' Deposit Linked Insurance (EDLI) for life cover. Understanding how to manage these accounts and navigate the withdrawal process is essential for securing your financial future.

The Role of the Employees' Provident Fund Organization in India’s Social Security Framework

EPFO is a government-backed system that helps employees save money for retirement in a safe and structured way. Unlike stock market investments, EPF is low-risk and gives fixed returns every year, making it a preferred choice for long-term savings. Its primary objective is to ensure that every worker in the organized sector has a financial safety net. Unlike volatile market investments, the EPF offers a guaranteed interest rate-currently set at 8.25% for the 2023-24 financial year—making it a preferred choice for risk-averse investors looking for long-term compounding benefits.

Decoding the EPFO Trifecta: Understanding the EPF, EPS, and EDLI Schemes

When you look at your salary slip, you see a deduction for 'PF.' However, that deduction fuels three distinct schemes designed to protect you at different stages of life:

- Employees' Provident Fund (EPF): This is your main savings pool. The money here earns annual interest and can be withdrawn as a lump sum upon retirement or during specific emergencies.

- Employees' Pension Scheme (EPS): This portion is designed to provide a monthly pension after you reach the age of 58, provided you have completed at least 10 years of eligible service.

- Employees' Deposit Linked Insurance (EDLI): This is a life insurance cover provided to all EPF members. In the unfortunate event of the member's death while in service, the nominee receives a lump sum payment of up to ₹7 Lakhs, based on the average salary of the deceased.

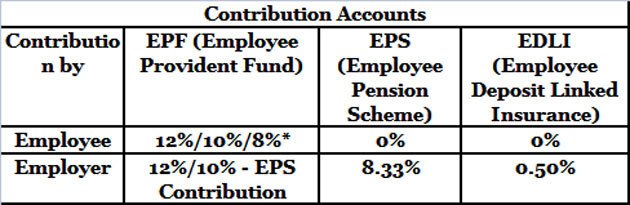

Analyzing Contribution Dynamics: How Monthly Deductions are Allocated

Every month, both you and your employer contribute to your PF. In most cases, 12% of your basic salary is deducted from your side, and your employer also adds their share. But many employees don’t realize that employer money is split between pension and PF savings.

- Your Contribution (12%): Entirely goes into your EPF account.

- Employer's Contribution (12%):

- 3.67% goes into your EPF account.

- 8.33% (capped at a wage ceiling of ₹15,000, which equals ₹1,250) goes into the EPS (Pension) pool.

- The employer also pays an additional 0.50% towards the EDLI scheme.

This structure ensures that while you build a liquid corpus in the EPF, you are also simultaneously funding a lifelong pension through the EPS.

The Universal Account Number (UAN): Activating Your Digital Identity

In the past, changing jobs meant the headache of transferring PF balance from one account number to another. The Universal Account Number (UAN) changed that. UAN is your permanent PF number that stays the same even if you change jobs. Without UAN, managing PF from multiple companies becomes very difficult.

To activate your UAN:

- Visit the EPFO Member Portal.

- Click on 'Activate UAN' under the 'Important Links' section.

- Enter your UAN, Aadhaar number, name, and date of birth as per records.

- Verify using the OTP sent to your Aadhaar-linked mobile number.

Once activated, you can download your passbook, update KYC, and track your balance in real-time.

Strategic Guide to EPF Withdrawals: Partial Advances and Final Settlements

While the EPF is a retirement tool, the EPFO allows members to withdraw funds early under specific circumstances. These are categorized into 'Partial Withdrawals' (Advances) and 'Final Settlements.'

1. Partial Withdrawals (Non-Refundable Advances)

You don't have to wait until retirement to access your funds for critical life events. Common grounds for advances include:

- Marriage: Up to 50% of the employee's contribution (requires 7 years of service).

- Education: For self or children's post-matriculation studies (requires 7 years of service).

- Medical Emergencies: For major surgeries or hospitalization of self or family members (no minimum service required).

- Home Purchase/Construction: Significant portions can be withdrawn for buying a house or land (requires 5 years of service).

2. Final Settlement

You can withdraw the full amount (EPF + EPS) if you have retired (age 58) or if you have been unemployed for more than two months. If you are switching jobs, it is always recommended to transfer the balance rather than withdraw it, to maintain the continuity of service for pension benefits.

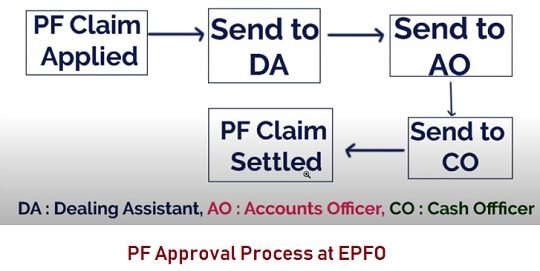

Step-by-Step Procedure for Filing Online EPF Claims

The days of submitting physical forms to the PF office are largely over. You can now file claims directly through the Unified Member Portal.

- Login: Access the portal using your UAN and password.

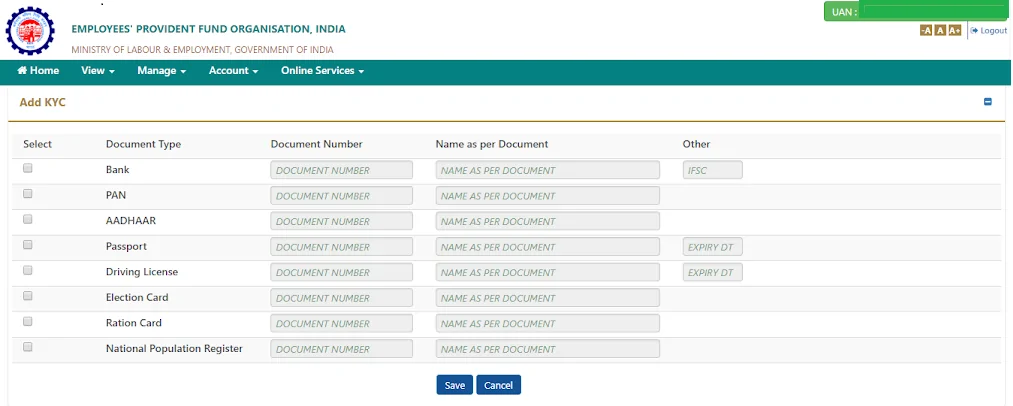

- Check KYC: Ensure your Aadhaar, PAN, and Bank details are 'Verified' under the 'Manage' tab.

- Select Claim: Go to 'Online Services' and select 'Claim (Form-31, 19, 10C & 10D)'.

- Verify Bank Account: Enter the last four digits of your linked bank account to verify.

- Select Form: Choose the type of withdrawal (e.g., Form 19 for full settlement, Form 31 for partial advance).

- Submit: Upload a scanned copy of a cancelled cheque or passbook and authenticate via Aadhaar OTP.

Taxability of EPF Withdrawals: The Five-Year Rule

One of the biggest advantages of the EPF is its tax status. However, there is a catch. To enjoy tax-free withdrawals, you must complete five years of continuous service.

- If you withdraw before 5 years: If you withdraw PF before completing 5 years of service, you may have to pay tax on it. But if you stay invested for 5 years or more, the entire amount becomes tax-free, which is one of the biggest advantages of EPF.

- If you withdraw after 5 years: The entire amount (principal + interest) is exempt from tax under Section 10(11) or 10(12) of the Income Tax Act.

Note: Service with different employers is considered 'continuous' if you transferred your PF balance from the old employer to the new one.

Common Hurdles in Claim Settlement

Many claims are rejected due to minor clerical errors. To ensure a smooth process, watch out for:

- KYC Mismatches: Ensure your name and date of birth on the EPFO portal exactly match your Aadhaar card. Even a spelling mistake like 'Suresh Kumar' vs 'Suresh Kr' can lead to rejection.

- Bank Account Issues: The bank account must be in your name (no joint accounts with anyone other than a spouse) and the IFSC code must be updated (especially after bank mergers).

- Signature Discrepancies: While most things are digital, if you use a physical form, the signature must match the records held by the employer.

Common Mistakes People Make

- Not linking Aadhaar with UAN

- Forgetting to transfer PF after job change

- Withdrawing PF too early

- Not checking employer contribution regularly

Frequently Asked Questions

1. Can I increase my contribution to the EPF?

Yes. Through the Voluntary Provident Fund (VPF), you can contribute more than the mandatory 12% of your basic salary. Your employer is not required to match this extra amount, but you get the same high interest rate.

2. What happens to my PF if I join a startup that doesn't have EPFO registration?

Your existing UAN remains valid. You can either let the money stay in the account (it will earn interest for 3 years of inactivity, but the interest will be taxable) or withdraw the amount if you remain unemployed by an EPFO-covered firm for 2 months.

3. How can I check my PF balance without logging into the portal?

You can send an SMS 'EPFOHO UAN ENG' to 7738299899 or give a missed call to 9966044425 from your registered mobile number.

4. Is it mandatory to link Aadhaar with UAN?

Yes, as per current regulations, Aadhaar linking is mandatory for the employer to file the monthly Electronic Challan-cum-Return (ECR) and for the employee to process online claims.

Conclusion: Securing Your Financial Future

The EPFO is more than just a monthly deduction; it is a disciplined investment vehicle that leverages the power of compounding. By ensuring your KYC is updated, your UAN is active, and your previous balances are transferred upon job changes, you turn a complex administrative requirement into a powerful retirement engine. Proactive management of your EPF today ensures that when you eventually hang up your professional boots, you have a substantial, tax-efficient corpus waiting to support your golden years.

Important Note: Financial Disclaimer: This guide is based on official EPFO rules, employee experiences, and commonly used withdrawal processes in India. It is written to help salaried employees understand how EPF works in real life, not just in theory.

Comments 0

Leave a Reply

Your email address will not be published. Required fields are marked *

Be the first to share your thoughts!