💡 Navigating the Complexities of Current Mortgage Rates: A Comprehensive Guide for Homebuyers

Understand the factors driving mortgage rate fluctuations and learn actionable strategies to secure the best possible terms for your home loan.

Mortgage rates represent the interest charged on a home loan, and they directly impact how much a buyer pays over time. These rates change based on inflation, Federal Reserve policy, and bond market trends. Even a small shift in rates can significantly affect monthly EMI and total repayment cost.

Why Mortgage Rates Matter for Homebuyers

Interest rate is one of the biggest factors in deciding the total cost of a home loan. It affects both monthly payments and long-term affordability. While the purchase price of a house is a fixed number, the interest rate dictates how much you actually pay for that house over 15 or 30 years. When rates are low, your purchasing power increases, allowing you to afford a more expensive home for the same monthly payment. Conversely, when rates rise, your budget may shrink as more of your monthly income is diverted toward interest rather than the principal balance of the loan.

The Economic Engines Driving Today’s Mortgage Rate Fluctuations

Mortgage rates change due to several key economic factors. The most important ones are inflation, bond yields, and Federal Reserve policies.

- Inflation: This is the primary driver of mortgage rates. When inflation is high, the purchasing power of the dollar drops. Lenders must charge higher interest rates to compensate for the fact that the money they are paid back in the future will be worth less than it is today.

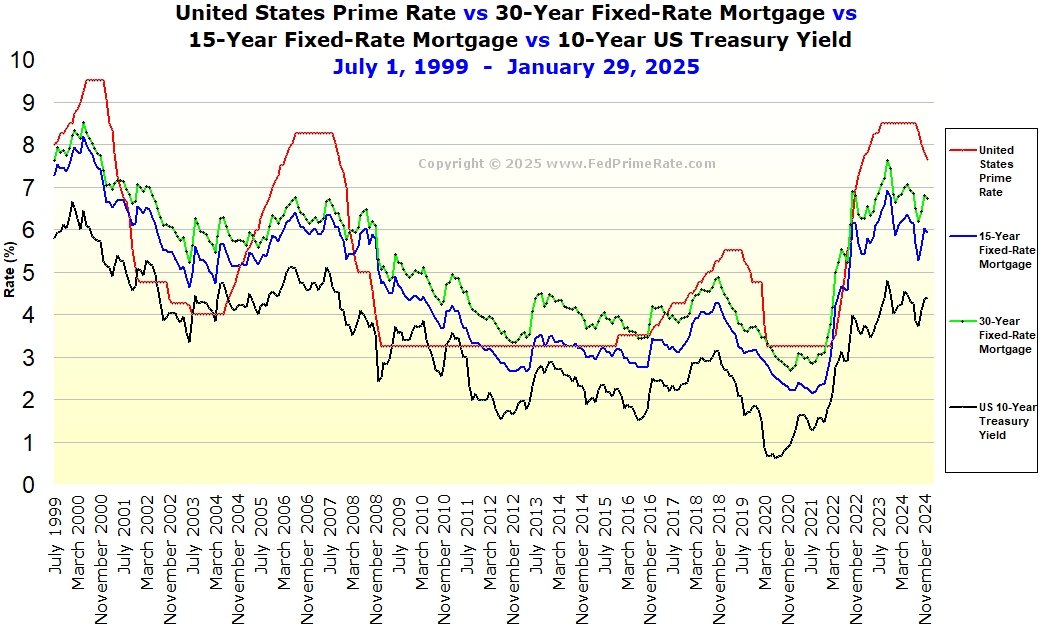

- The 10-Year Treasury Yield: Mortgage rates generally follow the trend of the 10-year Treasury note. When investors feel the economy is risky, they buy bonds, which lowers yields and often brings mortgage rates down. When the economy is booming, yields rise, and mortgage rates typically follow.

- The Federal Reserve: While the Fed does not set mortgage rates directly, its decisions on the federal funds rate influence the entire lending environment. When the Fed raises rates to combat inflation, mortgage lenders usually raise their rates in anticipation.

Comparing Fixed-Rate and Adjustable-Rate Mortgages in a Volatile Market

Choosing the right loan structure is just as important as the rate itself. The two most common options offer different levels of risk and reward.

Fixed-Rate Mortgages: These are the gold standard for stability. Your interest rate remains the same for the entire duration of the loan (usually 15 or 30 years). This protects you from future rate hikes but means you won't benefit if market rates drop unless you choose to refinance, which involves new closing costs.

Adjustable-Rate Mortgages (ARMs): These loans typically offer a lower "teaser" rate for an initial period (like 5, 7, or 10 years). After that, the rate adjusts periodically based on market conditions. ARMs can be beneficial if you plan to sell the home or refinance before the introductory period ends, but they carry the risk of significantly higher payments if rates rise in the future.

How to Get a Lower Mortgage Rate

Lenders reserve their best rates for the borrowers they perceive as the lowest risk. You can improve your standing by focusing on three key areas:

- Credit Score: A credit score above 760 usually helps you get the best mortgage rates. Even small improvements in your score can reduce your interest rate.

- Debt-to-Income (DTI) Ratio: This is the percentage of your gross monthly income that goes toward paying debts. Lenders prefer a DTI below 36%, though some programs allow higher. Lowering your DTI shows you have the cash flow to handle a mortgage.

- Down Payment: Putting 20% down not only eliminates the need for Private Mortgage Insurance (PMI) but also signals to the lender that you have significant "skin in the game," which can lead to a lower interest rate.

Interest Rate vs APR Explained

When comparing loan estimates, you will notice two numbers: the interest rate and the Annual Percentage Rate (APR). The interest rate is the cost of borrowing the principal. The APR is a broader measure that includes the interest rate plus other costs, such as broker fees, closing costs, and "points."

Discount Points: You can choose to "buy down" your interest rate by paying extra money upfront at closing. One point typically costs 1% of the loan amount and lowers your interest rate by about 0.25%. This is a great strategy if you plan to stay in the home long-term, as the monthly savings will eventually outweigh the upfront cost.

When to Lock Your Mortgage Rate

Once you apply for a mortgage, you have to decide whether to "lock" your rate or "float" it. A rate lock guarantees your interest rate for a specific period (usually 30 to 60 days) while your loan is processed.

- Locking: This is the safest move if you are happy with the current rate and believe rates might rise before you close.

- Floating: This means you wait to lock, hoping rates will drop before you close. This is risky; if rates spike, you are stuck with the higher cost. Floating is generally only recommended if market trends are clearly downward and you have a flexible closing date.

Frequently Asked Questions Regarding Current Lending Trends

1. Why are mortgage rates higher than the Fed's interest rate?

The Fed sets the short-term rate for banks to borrow from each other. Mortgage rates are long-term loans (15-30 years) and include a "risk premium" to account for inflation and the possibility of default over a much longer period.

2. Can I get a lower rate by choosing a 15-year mortgage?

Yes. 15-year mortgages almost always have lower interest rates than 30-year mortgages because the lender is taking on risk for a shorter period. However, your monthly payments will be significantly higher because you are paying off the principal much faster.

3. How often do mortgage rates change?

Mortgage rates can change daily, and sometimes even multiple times within a single day, depending on volatility in the bond market and economic news releases.

4. Does a pre-approval lock in my interest rate?

No. A pre-approval tells you how much you can borrow, but the interest rate isn't locked until you have a signed purchase agreement on a specific property and you formally request a lock from your lender.

Conclusion

Understanding mortgage rates helps homebuyers make better financial decisions. While market conditions change often, improving your credit score and choosing the right time to lock your rate can significantly reduce long-term costs. While you cannot control the Federal Reserve or inflation, you can control your credit score, your debt levels, and the timing of your rate lock. By understanding the relationship between economic engines and your personal financial profile, you can move from a place of uncertainty to one of empowerment, ensuring that your home investment is as affordable and sustainable as possible.

Comments 0

Leave a Reply

Your email address will not be published. Required fields are marked *

Be the first to share your thoughts!