💡 Navigating HDB Financial Services: A Comprehensive Guide to Personal and Business Credit Solutions

Discover the full range of credit solutions offered by HDB Financial Services, from personal and business loans to asset-backed lending and consumer durable financing in India.

HDB Financial Services (HDBFS) is a prominent Indian Non-Banking Financial Company (NBFC) that provides a wide array of credit solutions, including personal loans, business loans, commercial vehicle financing, and consumer durable loans. As a subsidiary of HDFC Bank, it serves both retail and commercial clients, focusing on providing accessible credit to individuals and small-to-medium enterprises (SMEs) across urban and semi-urban India. By leveraging a vast branch network and digital platforms, HDBFS bridges the gap for borrowers who may require more flexible eligibility criteria than traditional banks while maintaining the security of a reputable financial institution.

The Evolution of HDB Financial Services as a Leading NBFC

Since its incorporation in 2007, HDB Financial Services has evolved from a retail-focused lender into one of India’s largest and most diversified NBFCs. Unlike traditional banks that may have rigid bureaucratic layers, HDBFS was designed to be agile. Its growth is deeply rooted in its ability to reach the "missing middle"—borrowers who are creditworthy but often overlooked by large private banks due to location or specific documentation challenges.

Today, the company operates as a systemically important non-deposit-taking NBFC. Its evolution is marked by a shift from physical-only processing to a hybrid model where technology speeds up the loan lifecycle, from application to disbursement. This evolution has allowed it to maintain a massive loan book while diversifying into niche segments like construction equipment and gold loans.

The Strategic Role of HDBFS in India’s Retail and Commercial Credit Landscape

In the broader Indian economy, HDBFS plays a critical role in driving financial inclusion. It acts as a conduit for credit in regions where HDFC Bank might not have a full-service branch but where credit demand is high. By focusing on both secured and unsecured lending, HDBFS helps stabilize the credit ecosystem, providing liquidity to small businesses and individual consumers alike.

Tailored Personal Credit: Exploring Personal Loans and Lifestyle Financing

For individuals, HDBFS offers personal loans that are designed for versatility. Whether it is for a wedding, a medical emergency, home renovation, or international travel, these loans are typically unsecured, meaning no collateral is required.

Key Features:

- Loan Amounts: Flexible limits based on repayment capacity.

- Tenure: Usually ranges from 12 to 60 months.

- Speed: Faster processing times compared to traditional home or auto loans.

Limitations: While convenient, personal loans often carry higher interest rates than secured loans (like home loans). Borrowers with lower credit scores may also find the interest rates significantly higher, making it essential to compare the Total Cost of Credit before signing.

Fueling Entrepreneurship: Specialized Business Loans and SME Credit Facilities

Small and Medium Enterprises (SMEs) are the backbone of the Indian economy, yet they often face a "credit gap." HDBFS addresses this through specialized business loans. These are aimed at providing working capital, funding expansion, or purchasing inventory. They offer both secured business loans (against property) and unsecured business loans for established entities.

For a small manufacturer or a retail shop owner, these loans provide the necessary cash flow to manage seasonal demands. HDBFS looks at the business's turnover and banking history rather than just tax returns, which helps many self-employed professionals qualify.

Asset-Backed Lending: Commercial Vehicle and Construction Equipment Financing

One of the strongest pillars of HDBFS is its asset-backed lending division. This segment focuses on the transport and infrastructure sectors. They provide financing for:

- Commercial Vehicles: New and used trucks, tippers, and buses.

- Construction Equipment: Backhoe loaders, excavators, and cranes.

This is vital for contractors and fleet owners who need expensive machinery to execute projects but cannot afford the upfront capital expenditure. By using the equipment itself as collateral, HDBFS enables these entrepreneurs to grow their operations incrementally.

The Digital Shift: Consumer Durable Loans and Instant Credit Solutions

HDBFS has heavily invested in the "Buy Now, Pay Later" (BNPL) trend through its consumer durable loans. When you walk into an electronics store to buy a smartphone, washing machine, or laptop, HDBFS often provides the point-of-sale financing. These are often marketed as "No Cost EMI" deals, though it is important to check for processing fees that might be hidden in the fine print.

Understanding the HDBFS Advantage: Interest Rates, Tenure, and Flexibility

The primary advantage of choosing HDBFS is the flexibility in documentation. They are often more willing to look at surrogate income proofs (like bank statements or repayment tracks of previous loans) than some public sector banks.

Advantages:

- Wide geographical reach across India.

- Transparent digital tracking of loan accounts via their app.

- Quick turnaround time (TAT) for loan approvals.

Limitations:

- Interest rates can be higher than those offered by parent company HDFC Bank for prime customers.

- Customer service experiences can vary significantly between urban and rural branches.

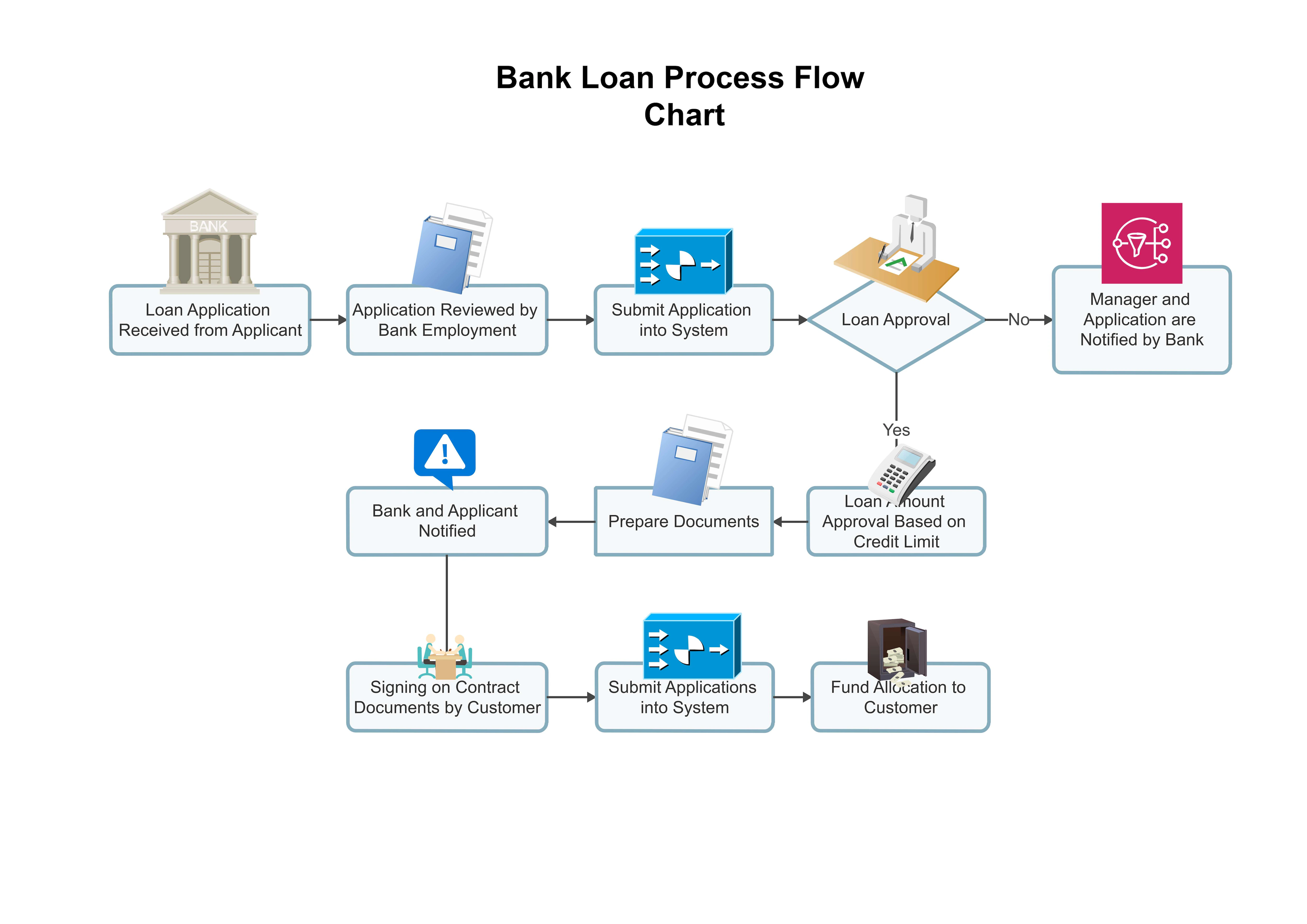

Navigating the Application Journey: Documentation and Eligibility Criteria

Applying for a loan at HDBFS is a straightforward process, but being prepared with documentation is key to a smooth experience.

Commonly Required Documents:

- Identity Proof: Aadhaar Card, PAN Card, or Voter ID.

- Address Proof: Utility bills or rent agreements.

- Income Proof: Salary slips for employees; Bank statements and ITR for self-employed individuals.

- Business Proof: GST registration or Trade License (for business loans).

The eligibility is largely determined by your CIBIL score and your Fixed Obligation to Income Ratio (FOIR), which measures how much of your monthly income is already going toward existing debts.

Frequently Asked Questions Regarding HDB Financial Services

1. Is HDB Financial Services the same as HDFC Bank?

No, HDB Financial Services is a subsidiary of HDFC Bank. While they share a parentage and high standards of governance, HDBFS operates as a separate NBFC with its own products, interest rates, and target customer segments.

2. Can I get a loan from HDBFS if I am self-employed?

Yes, HDBFS has specific products tailored for self-employed professionals and non-professionals, focusing on business turnover and banking habits rather than just fixed salaries.

3. How can I pay my HDBFS loan EMIs?

Payments can be made via National Automated Clearing House (NACH) mandates, the HDBFS mobile app, their official website, or through various digital wallets and UPI platforms.

4. Does HDBFS charge a penalty for early loan closure?

Yes, most NBFCs, including HDBFS, charge a foreclosure fee if you pay off your loan before the end of the tenure. This fee typically ranges from 2% to 4% of the principal outstanding, depending on the specific loan agreement.

Conclusion: Choosing the Right Financial Partner for Your Growth Journey

HDB Financial Services stands as a robust alternative to traditional banking for millions of Indians. Its strength lies in its diverse product portfolio—covering everything from a small mobile phone purchase to heavy industrial machinery. While the interest rates might be slightly higher than those of a standard bank loan, the ease of access, faster processing, and flexible eligibility make it a strategic choice for those looking to fuel their personal or professional growth. As with any financial commitment, potential borrowers should carefully read the terms and conditions, understand the fee structure, and ensure that the EMI fits comfortably within their monthly budget.

Important Note: Financial Disclaimer: This content is for educational purposes only and does not constitute professional financial advice. Always consult with a certified financial planner before making investment decisions.

Comments 0

Leave a Reply

Your email address will not be published. Required fields are marked *

Be the first to share your thoughts!