💡 Trump Accounts for Kids: A Strategic Financial Analysis

An authoritative guide on custodial accounts, tax strategies, and wealth transfer for minors under current legislative frameworks.

Executive Summary

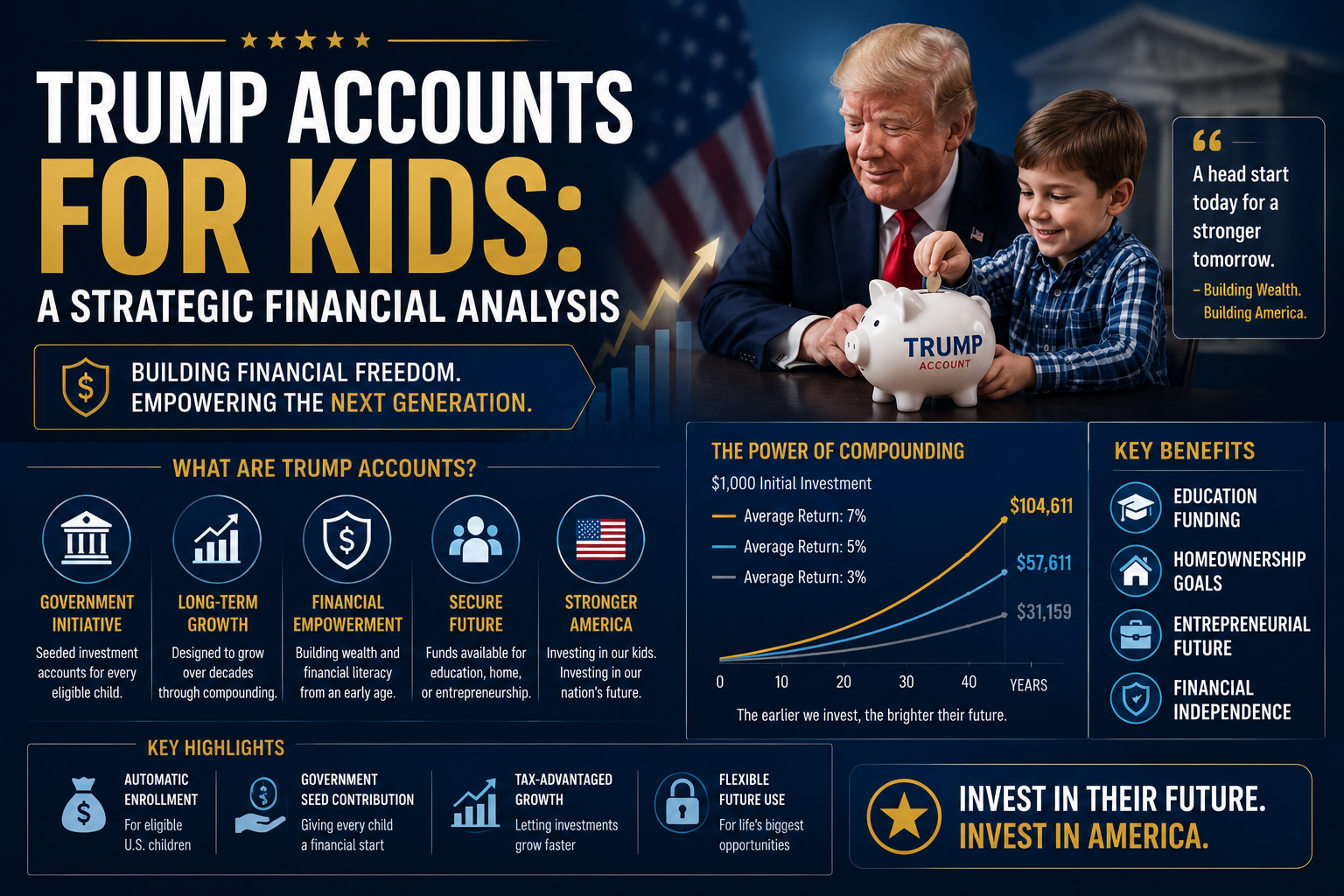

Strategic financial planning for minors has undergone significant shifts due to the Tax Cuts and Jobs Act (TCJA) and subsequent legislative updates. This analysis examines the mechanics of custodial accounts, the evolving Kiddie Tax regulations, and the strategic utilization of 529 plans. Key data highlights include the 2024 annual gift tax exclusion of 18,000 dollars and the 2,600 dollar threshold for unearned income taxation. This report provides a roadmap for high net worth individuals and middle class families to optimize wealth transfer while maintaining compliance with federal tax codes.

Introduction

The landscape of generational wealth transfer is often dictated by the prevailing tax policies of the era. The term Trump accounts for kids frequently refers to the financial structures and custodial vehicles optimized under the Tax Cuts and Jobs Act of 2017. This legislation fundamentally altered how unearned income for minors is treated, creating both opportunities and pitfalls for parents and guardians. Understanding these accounts requires a sophisticated grasp of tax law, investment strategy, and long term estate planning. As the global economy reacts to shifts in the Stock Market Today: Strategic Analysis of Global Trends, establishing a robust foundation for the next generation has never been more critical.

The Deep Dive: Legislative Framework and Account Structures

To understand the strategic value of these accounts, one must first analyze the primary vehicles used for minor beneficiaries. These include Uniform Transfers to Minors Act (UTMA) accounts, Uniform Gifts to Minors Act (UGMA) accounts, and 529 Qualified Tuition Programs. Each carries distinct tax implications and control mechanisms.

The Evolution of the Kiddie Tax

The Kiddie Tax was originally designed to prevent parents from shifting large amounts of investment income to children in lower tax brackets. Under the TCJA, the taxation of a child’s unearned income was briefly tethered to the brackets used for trusts and estates. However, subsequent revisions have reverted this to the parents marginal tax rate. For the 2024 tax year, the following breakdown applies:

- The first 1,300 dollars of unearned income is covered by the child’s standard deduction and is tax free.

- The next 1,300 dollars is taxed at the child’s individual tax rate, which is typically 10 percent.

- Unearned income exceeding 2,600 dollars is taxed at the parents marginal tax rate.

This structure necessitates a careful balance of asset allocation to ensure that the tax drag does not negate the benefits of early investment. Families must consider how corporate shifts, such as those seen in Byju's Strategy and Corporate Governance: A Strategic Analysis, might impact the long term viability of specific educational or growth focused investments.

Strategic Use of 529 Plans and Roth IRA Rollovers

One of the most significant strategic developments in recent years is the ability to roll over unused 529 plan funds into a Roth IRA for the beneficiary. This provision, introduced via the SECURE 2.0 Act, allows for a lifetime maximum rollover of 35,000 dollars. This effectively mitigates the risk of overfunding an educational account if the child receives scholarships or chooses a different career path. To qualify, the account must have been open for at least 15 years, and the funds must have been in the account for at least five years.

Gift Tax Exclusions and Lifetime Exemptions

High net worth individuals often utilize the annual gift tax exclusion to fund these accounts. In 2024, an individual can gift up to 18,000 dollars per child without triggering a gift tax return or reducing their lifetime gift and estate tax exemption. For married couples, this amount doubles to 36,000 dollars. This strategy is a cornerstone of aggressive wealth transfer, allowing families to move significant assets out of their taxable estate while the assets are still at a lower valuation.

What This Means For You

For the average investor or parent, the complexity of these accounts can be simplified into actionable steps. First, determine the primary goal of the account. If the goal is strictly education, a 529 plan offers the most aggressive tax advantages. If the goal is general wealth building or providing a down payment for a future home, a UTMA or UGMA account provides more flexibility, albeit with less tax protection for high levels of unearned income.

- Identify your tax bracket: If you are in a high marginal bracket, keep unearned income below the 2,600 dollar threshold to avoid the Kiddie Tax.

- Leverage the 15 year rule: Open 529 plans early to take advantage of the SECURE 2.0 Roth IRA rollover provisions later.

- Monitor asset location: Place tax efficient assets, like low turnover index funds, in custodial accounts to minimize annual capital gains distributions.

Expert Verdict and Future Outlook

The future of accounts for minors is likely to be shaped by the potential expiration of many TCJA provisions in 2025. Financial experts anticipate a period of volatility in tax planning as legislators debate whether to extend the current individual income tax rates and the heightened estate tax exemption. Currently, the lifetime estate tax exemption stands at an unprecedented 13.61 million dollars per individual. If this sunset occurs, the strategic importance of early and consistent gifting to accounts for kids will increase significantly. Investors should remain agile and consult with tax professionals to adjust their strategies as new federal budgets are proposed.

FAQ

What is the main difference between a UTMA and a 529 plan?

A UTMA account is a custodial account that can hold almost any asset, including real estate and stocks, and the funds can be used for any purpose that benefits the minor. A 529 plan is specifically designed for education expenses and offers tax free growth and withdrawals for qualified educational costs.

Can I withdraw money from my childs custodial account for my own use?

No. Once funds are deposited into a UTMA or UGMA account, they become the legal property of the minor. The custodian has a fiduciary duty to manage the funds solely for the benefit of the child. Misuse of these funds can lead to legal and tax penalties.

How does the Kiddie Tax affect my childs part time job income?

The Kiddie Tax only applies to unearned income, such as interest, dividends, and capital gains. Earned income from a job is taxed at the childs standard individual income tax rate and is not subject to the parents marginal rate.

At what age does the child gain control of a UTMA account?

The age of majority or termination varies by state, typically ranging from 18 to 21. At this point, the custodian must transfer the assets to the child, who then has full control over how the money is spent.

Is there a limit on how much I can contribute to a 529 plan?

While there are no annual contribution limits set by the federal government, each state has an aggregate limit for 529 plans, often ranging from 235,000 to over 500,000 dollars. Additionally, contributions are subject to gift tax rules.

Conclusion

Navigating the strategic landscape of financial accounts for minors requires a proactive approach to tax law and investment management. By leveraging the current benefits of the TCJA and the SECURE 2.0 Act, parents can create a powerful financial legacy. The key takeaway is to start early, utilize tax advantaged vehicles like 529 plans, and remain mindful of the thresholds that trigger the Kiddie Tax. As legislative environments change, the flexibility and foresight built into these accounts today will determine the financial security of the next generation tomorrow.

Important Note: Financial Disclaimer: This content is for educational purposes only and does not constitute professional financial advice. Always consult with a certified financial planner before making investment decisions.

Comments 0

Leave a Reply

Your email address will not be published. Required fields are marked *

Be the first to share your thoughts!