💡 Investing in Sun Pharmaceutical Industries: A Comprehensive Guide to Performance, Growth Drivers, and Market Outlook

A comprehensive analysis of Sun Pharmaceutical Industries, exploring its shift toward specialty medicines, financial health, and long-term investment potential in the global healthcare market.

Sun Pharmaceutical Industries is India’s largest pharmaceutical company and a dominant force in the global generic and specialty medicine markets. For investors, the Sun Pharma share represents a balanced exposure to stable domestic earnings in India and high-growth specialty segments in the United States. Its recent moves, including the multi-billion dollar acquisition of Organon’s business, signal a transition from a traditional generic manufacturer to a global specialty powerhouse. While the stock offers strong long-term growth potential and robust cash flows, its performance is often sensitive to USFDA regulatory actions and currency fluctuations in emerging markets.

The Dominance of Sun Pharma in the Global Healthcare Landscape

Sun Pharma occupies a unique position as the fourth-largest specialty generic pharmaceutical company in the world. Unlike many of its peers that rely solely on low-margin generic drugs, Sun Pharma has successfully diversified its portfolio across 100+ countries. In India, it holds a market share of approximately 8%, making it the leader in the domestic formulation segment. This leadership is built on a foundation of chronic therapy dominance, particularly in specialties like cardiology, neurology, and gastroenterology.

The Strategic Evolution: From Niche Player to Global Leader

The journey of Sun Pharma is defined by aggressive inorganic growth and a pivot toward complex therapeutics. Starting as a small psychiatry-focused firm in 1983, it grew through a series of strategic acquisitions, most notably the Ranbaxy merger in 2014. Today, the company is undergoing its most significant evolution yet: the shift toward "Specialty Medicines." This involves developing branded products for specific conditions like plaque psoriasis, dry eye disease, and severe acne. The recent $11.75 billion deal to acquire assets from Organon further cements this strategy, positioning Sun Pharma as a major player in women’s health and biosimilars, categories that offer higher entry barriers and better pricing power than standard generics.

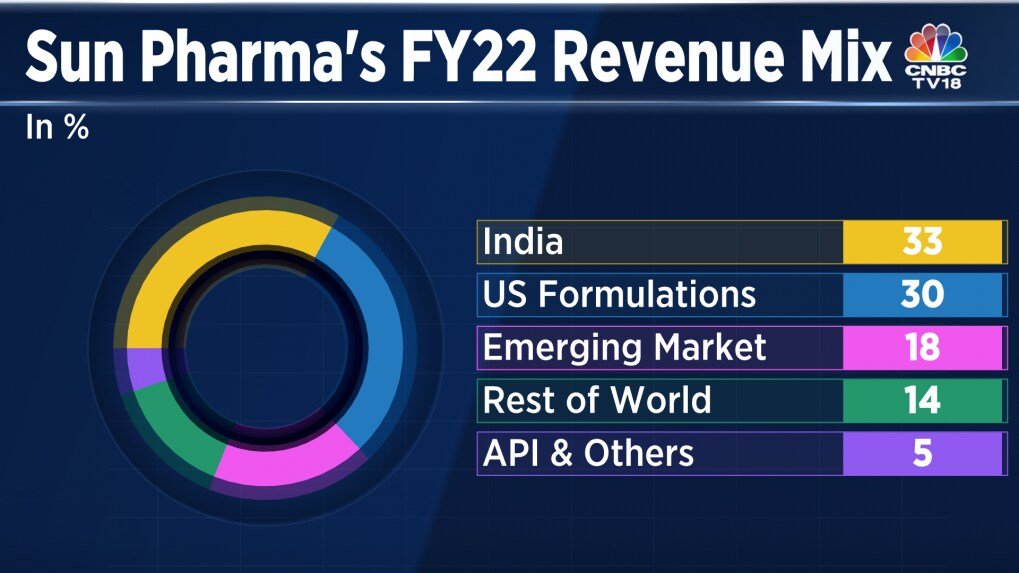

Analyzing the Revenue Mix: The Shift Toward Specialty Medicines

To understand the Sun Pharma share price, one must look at the changing composition of its revenue. Historically, the company was a volume-driven generic player. Today, its revenue is divided into four main pillars:

- India Formulations: Providing steady, inflation-linked growth with high brand loyalty.

- US Business: Driven increasingly by specialty brands like Ilumya, Cequa, and Winlevi, which now contribute a significant portion of US sales.

- Emerging Markets: Growth across 80+ countries including Brazil, Mexico, and Russia.

- Rest of World (RoW): Including Western Europe, Canada, and Australia.

- APIs (Active Pharmaceutical Ingredients): Ensuring vertical integration and supply chain security.

The specialty segment is the most critical driver for future valuation. Because these products are patent-protected or require complex manufacturing, they are less prone to the price erosion that typically plagues the US generic market.

Financial Health Assessment: Key Metrics

Sun Pharma maintains a healthy balance sheet, which is a primary reason for its premium valuation compared to other Indian pharma stocks. Key metrics to monitor include:

- EBITDA Margins: The company consistently aims for margins in the 22-25% range, supported by the high-margin specialty portfolio.

- Debt-to-Equity: Sun Pharma has historically maintained low debt levels, allowing it the flexibility to pursue large-scale acquisitions without overleveraging.

- Cash Flow: Strong internal accruals fund its massive R&D budget, which typically hovers around 7-8% of total sales.

The R&D Engine: Innovation and Pipeline Development

Innovation is the insurance policy for any pharmaceutical investment. Sun Pharma invests heavily in its R&D engine, focusing on complex generics and New Chemical Entities (NCEs). The company currently has a robust pipeline of ANDAs (Abbreviated New Drug Applications) pending with the USFDA. Beyond generics, its focus on clinical trials for new indications of existing specialty drugs ensures that the lifecycle of its high-value products is extended, protecting revenue streams from future competition.

Navigating the Regulatory Landscape: USFDA Compliance

One of the primary risks associated with the Sun Pharma share is regulatory volatility. Like all major drugmakers exporting to the US, Sun Pharma’s manufacturing facilities are subject to rigorous USFDA inspections. Issues at key plants, such as Halol or Mohali, have historically led to Import Alerts or Warning Letters, which temporarily halt new product approvals from those sites. Investors must keep a close watch on "Form 483" observations, as these are often the first sign of potential regulatory hurdles that could impact short-term stock performance.

Macroeconomic Factors and External Pressures

As a global entity, Sun Pharma is exposed to external pressures beyond its control:

- Currency Fluctuations: Since a large portion of revenue is earned in USD and other foreign currencies, a strengthening Rupee can negatively impact reported earnings.

- Input Costs: Rising prices for raw materials (APIs) and energy can squeeze margins if not passed on to consumers.

- Healthcare Policy: Changes in US healthcare laws or drug pricing regulations can impact the profitability of the generic segment.

Investment Thesis: A Long-Term Core Portfolio Asset

Investing in Sun Pharma is essentially a bet on the professionalization and specialization of Indian healthcare.

Advantages:

- Market leadership in the high-growth Indian chronic care segment.

- Reduced dependence on commoditized generics through specialty drug success.

- Strong track record of integrating large acquisitions.

Limitations:

- High sensitivity to USFDA compliance and inspection outcomes.

- Intense competition in the generic space leading to price erosion.

- Valuation premiums make it more expensive than some of its peers.

Frequently Asked Questions

1. Does Sun Pharma pay regular dividends?

Yes, Sun Pharma has a consistent track record of paying dividends to its shareholders, supported by its strong free cash flow and stable earnings from the Indian market.

2. How does the US market impact the Sun Pharma share price?

The US is Sun Pharma's largest market outside India. Growth in specialty drug sales in the US typically drives the share price upward, while regulatory hurdles or generic price erosion act as headwinds.

3. What makes Sun Pharma different from other Indian pharma companies?

Sun Pharma is distinguished by its successful transition into branded specialty medicines in the US, whereas many other Indian firms remain primarily focused on low-margin generic drugs.

4. Is Sun Pharma a defensive stock?

Generally, yes. The pharmaceutical sector is considered defensive because the demand for medicine remains relatively stable regardless of economic downturns.

5. What is the significance of the Organon deal?

The acquisition of Organon's business is a strategic move to dominate the women's health and biosimilar market, providing a new long-term growth engine for the company.

Important Note: Financial Disclaimer: This content is for educational purposes only and does not constitute professional financial advice. Always consult with a certified financial planner before making investment decisions.

Conclusion

Sun Pharmaceutical Industries remains a cornerstone of the Indian healthcare sector and a formidable global competitor. Its strategic pivot toward specialty medicines has successfully de-risked the business from the volatility of the generic drug market. While regulatory challenges and currency risks remain ever-present, the company’s strong domestic leadership, robust R&D pipeline, and healthy balance sheet make it a compelling choice for long-term investors. As Sun Pharma continues to integrate massive acquisitions like Organon, its ability to maintain high margins and navigate global compliance standards will be the primary determinants of its future share performance.

Comments 0

Leave a Reply

Your email address will not be published. Required fields are marked *

Be the first to share your thoughts!