💡 Mortgage Market Strategic Analysis: 2024-2025 Trends

A high-authority breakdown of current mortgage trends, interest rate forecasts, and strategic financial planning for the 2024-2025 housing market.

Executive Summary

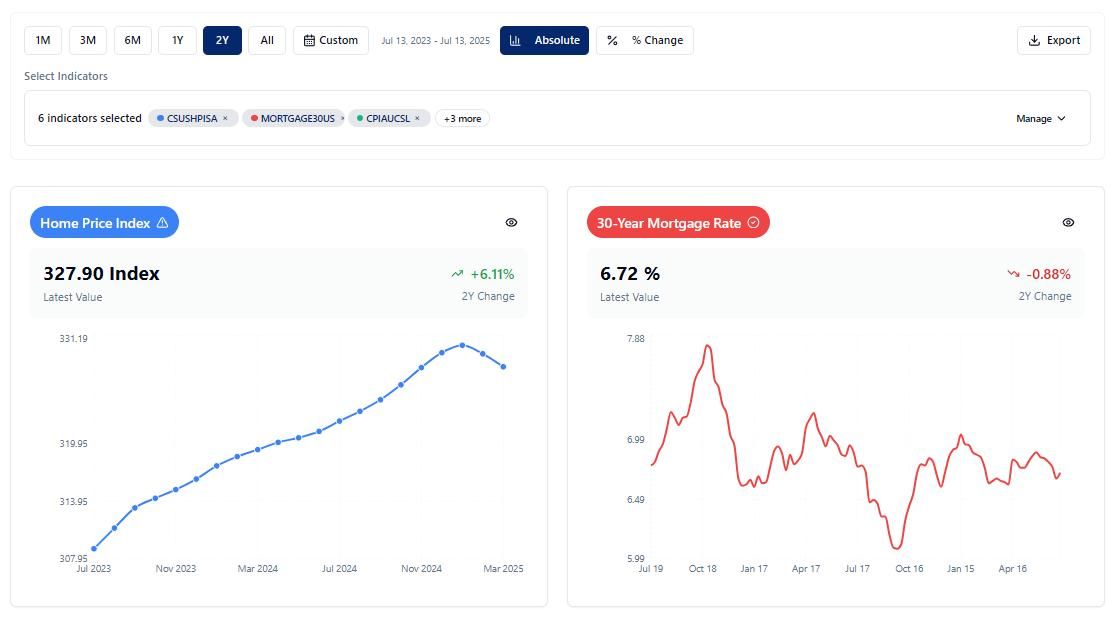

The global mortgage landscape is currently experiencing a period of significant recalibration following the aggressive monetary tightening cycles of 2022 and 2023. As of late 2024, the 30-year fixed-rate mortgage remains the primary vehicle for residential debt, with rates stabilizing between 6.5 percent and 7.2 percent. Key findings indicate that while inventory remains tight, the demand for purchase-money mortgages is showing resilience among high-credit-score borrowers. This analysis highlights a shift toward digital-first origination, the rising importance of debt-to-income (DTI) management, and the emergence of green mortgages as a sustainable finance tool. Data from the Federal Reserve and Freddie Mac suggests that while a return to the 3 percent era is unlikely, the market is finding a new equilibrium that favors strategic, well-capitalized buyers.

Introduction

A mortgage is more than a simple loan for a home; it is a complex financial instrument that serves as the bedrock of the global credit market. For the individual consumer, it represents the largest single liability they will likely manage. For the broader economy, mortgage-backed securities (MBS) provide essential liquidity to the financial system. Understanding the mechanics of these loans requires an analytical perspective on interest rate policy, credit risk assessment, and macroeconomic trends. The current environment is defined by a transition from the era of free money to a period of normalized interest rates, forcing both lenders and borrowers to adopt more sophisticated financial strategies. This report examines the structural components of modern mortgages and provides a roadmap for navigating the complexities of the current credit cycle.

THE DEEP DIVE: Mechanics and Macroeconomic Drivers

The primary driver of mortgage rates is the yield on the 10-year Treasury note, which is influenced by the Federal Open Market Committee (FOMC) decisions and inflation expectations. When inflation remains above the 2 percent target, the Federal Reserve maintains higher benchmark rates, which pushes mortgage spreads wider. Currently, the spread between the 10-year Treasury and the 30-year fixed mortgage is wider than historical averages, reflecting market volatility and lender risk aversion.

Digital transformation has fundamentally altered the mortgage origination process. The move toward automated underwriting systems (AUS) and electronic closing (eClosing) has reduced the average time to close from 50 days to approximately 35 days in efficient operations. This shift mirrors the broader movement toward data-driven governance seen in other sectors, such as the Self Enumeration Census: A Strategic Digital Transformation Analysis, where digital accessibility and data integrity are paramount. Modern lenders now use Application Programming Interfaces (APIs) to verify income, employment, and assets in real-time, reducing the risk of fraud and improving the borrower experience.

Another critical factor is the integration of Environmental, Social, and Governance (ESG) criteria into lending practices. Financial institutions are increasingly offering preferential rates for energy-efficient homes, a trend aligned with global Climate Strategy & Sustainability Trends. These green mortgages reward borrowers for reducing their carbon footprint, acknowledging that energy-efficient properties often have lower default risks due to reduced utility costs for the occupant.

Credit scoring remains the gatekeeper of mortgage affordability. A borrower with a FICO score of 760 or higher can expect to pay significantly less in interest over the life of a loan compared to a borrower in the 620 to 660 range. For a 400,000 dollar loan, this difference can exceed 100,000 dollars in total interest paid. Furthermore, the debt-to-income ratio is being scrutinized more heavily. While conventional loans allow for a DTI of up to 43 percent, many lenders are tightening internal overlays to 36 percent to mitigate the risk of a potential economic slowdown.

The competitive landscape of the mortgage industry is also shifting. Non-bank lenders now originate more than 60 percent of all residential mortgages in the United States. This consolidation and the dominance of major fintech platforms in the lending space can be compared to the market saturation strategies observed in the media sector, such as Disney Plus: A Strategic Analysis of Streaming Dominance. Just as streaming platforms compete for subscriber retention through technology, mortgage lenders are competing through integrated financial ecosystems that provide insurance, banking, and real estate services under one digital roof.

WHAT THIS MEANS FOR YOU

Navigating the mortgage market requires a disciplined approach to personal finance. For prospective homeowners and those looking to refinance, the following actions are essential:

- Optimize Credit Before Application: Ensure your credit report is free of errors and keep credit utilization below 30 percent at least six months before applying for a pre-approval.

- Calculate Total Cost of Ownership: Move beyond the monthly principal and interest payment. Include property taxes, homeowners insurance, and a maintenance reserve of 1 percent of the home value annually.

- Evaluate Loan Types: Consider the trade-offs between a 30-year fixed rate for stability and a 5/1 or 7/1 Adjustable-Rate Mortgage (ARM) if you plan to relocate within a decade.

- Lock the Rate Strategically: In a volatile market, a 60-day rate lock can protect you from sudden spikes, even if it requires a small upfront fee.

- Manage Debt-to-Income: Avoid large purchases like new vehicles or expensive furniture on credit until after the mortgage has closed and the deed is recorded.

Expert Verdict / Future Outlook

The consensus among housing economists suggests that mortgage rates will remain in the 6 percent range through much of 2025. While the Federal Reserve may implement incremental rate cuts as inflation cools, the lack of housing inventory will likely keep home prices elevated. The future of the industry lies in hyper-personalization. We expect to see more algorithmic lending products that adjust rates based on a borrower's specific professional trajectory and spending patterns. Additionally, the secondary market for mortgages will likely see an increase in private-label securitization as banks seek to move assets off their balance sheets to comply with stricter capital requirements. For the consumer, the takeaway is clear: the era of reactive borrowing is over. Success in the current market requires a proactive, data-informed strategy.

FAQ

Is it better to get a fixed-rate or an adjustable-rate mortgage right now?

A fixed-rate mortgage offers long-term security in an uncertain economy. However, an ARM may be appropriate if you expect rates to drop significantly in the next few years, allowing you to refinance before the adjustment period begins. Most experts currently recommend fixed rates for primary residences.

What is the minimum down payment required for a mortgage?

While 20 percent is the standard to avoid Private Mortgage Insurance (PMI), many conventional programs allow for as little as 3 percent down. FHA loans require 3.5 percent, and VA loans offer 0 percent down options for eligible veterans and active-duty service members.

How does inflation affect my existing mortgage?

If you have a fixed-rate mortgage, inflation can actually benefit you. As the value of currency decreases, you are paying back your loan with dollars that are worth less than when you borrowed them, effectively reducing the real cost of your debt over time.

What is Private Mortgage Insurance (PMI) and how do I remove it?

PMI is a fee charged by lenders to protect them if you default on a loan with less than 20 percent equity. You can typically request to cancel PMI once your loan-to-value ratio reaches 80 percent, or it must be automatically terminated by the lender at 78 percent.

Can I get a mortgage with a high debt-to-income ratio?

It is possible, but difficult. Some programs allow for a DTI up to 50 percent with compensating factors like high cash reserves or a significant down payment, but you will likely face higher interest rates and stricter underwriting requirements.

Important Note: Financial Disclaimer: This content is for educational purposes only and does not constitute professional financial advice. Always consult with a certified financial planner before making investment decisions.

Conclusion

The mortgage market is currently defined by a return to historical norms and a heavy reliance on digital efficiency. While the days of sub-3 percent rates are in the past, the current environment offers stability for those who approach home financing with a strategic mindset. By focusing on credit health, understanding macroeconomic drivers, and leveraging digital tools, borrowers can secure financing that aligns with their long-term wealth-building goals. The strategic takeaway is that in a high-rate environment, the quality of the borrower's financial profile is the most significant lever for affordability.

Comments 0

Leave a Reply

Your email address will not be published. Required fields are marked *

Be the first to share your thoughts!